Accelerate your delivery cycle from several days to real-time with instant card payouts.

With real-time payments gaining momentum, ‘real-time’ and ‘instant’ delivery are increasingly growing to be part of the payments conversation. As a result, many businesses are reevaluating payments strategies in a bid to deliver faster payments at a lower cost. Card payouts are further starting to be recognized as a best-fit solution for those looking to optimize payout strategies due to their ability to align with these goals and deliver funds almost instantly. While this method is an efficient means to push payments, it is better fit for some programs more than others. Here, we’ll explore what card payouts are, how they work, the use cases that they best support, and where they fit in the Rapyd Disburse offering.

What Is a Card Payout?

Original Credit Transaction (OCT) is a direct payout method that has long been leveraged by merchants to issue refunds. Card payouts are a further productization of the OCT capability that extend the application of the refund use case for global payouts at large. It is a type of push payment that directs funds from a payment service provider to a cardholder account. Through card payouts, platforms can push payments to cards rather than exclusively to bank accounts – a process that delivers the value of speed via a faster time to payout.

How Card Payouts Differ from Refunds

Despite the fact that card refunds and card payouts use the same underlying technology, some key differences highlight the advantage of card payouts:

| Card Refunds | Card Payouts |

|

|

How Card Payouts Work

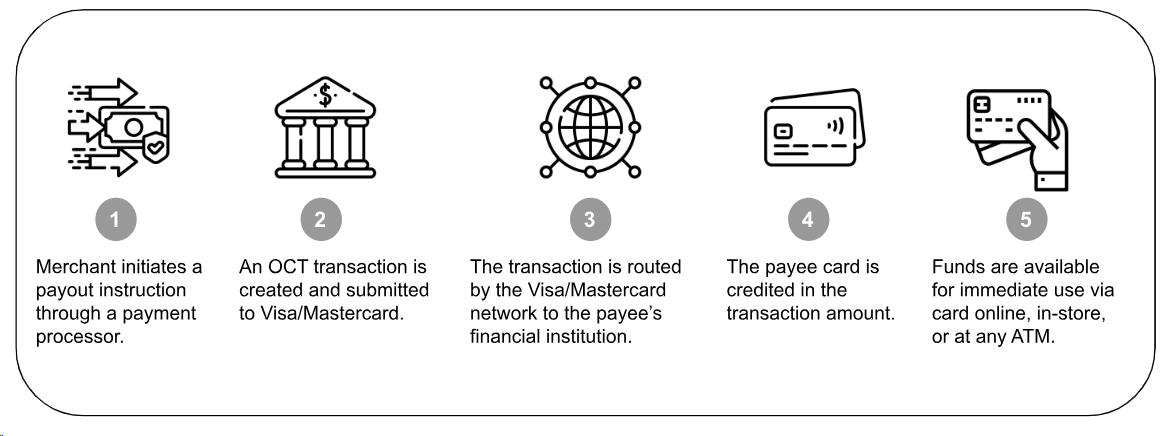

Card payouts are facilitated via Mastercard Send and Visa Direct. These infrastructures leverage debit and card scheme networks to move funds rather than traditional payments infrastructures like ACH rails. The process begins when a merchant initiates a payout through a payment processor like Rapyd using payee card (rather than bank account) details. This request is forwarded to the card-issuing bank via the card network (Mastercard or Visa) where it undergoes processing similar to a refund transaction whereby funds are pushed to the card rather than pulled from it. Once authorized, these funds are credited to the payee card, completing the payout. This service is made available by a payment processor through a unique set of APIs.

Benefits of card payouts

Card payouts offer several advantages to both the companies initiating payouts and their payees:

- Speed: Card payout transactions are processed in real-time, delivering funds almost instantly to payees.

- Simplicity: They deliver an improved customer experience by simplifying payee-facing processes, bypassing the need to register or onboard payees ahead of payout.

- Scale: Card payouts are built to support mass payouts at scale. Funds transfer APIs make it easy to automate payouts initiation and disbursement at high volumes and to process repeat payments.

- Security: Payments disbursed to cards are safe and secure since they leverage the infrastructure of legacy payments rails that uphold the highest security standards. Compliance-oriented APIs screen requests across watch lists to vet all payees involved in cross-border transactions.

Relevant use cases

Card payouts are best suited in B2C or C2C contexts where payouts are issued to individual entities – be it for payroll, rewards, winnings or earnings. They are less suited for B2B use cases since these are more operationally complex and often require more sophisticated reconciliation. The following table outlines use cases where card payouts are best fit to deliver funds to beneficiaries:

| Payout Type | Description | Industry use case | Example of fit |

| Earnings | Funds made through affiliate referrals, contract work, direct sales on marketplace platforms, or promotion of user generated content. | eCommerce |  |

| Content creation/Social media |  |

||

| Affiliate platforms |  |

||

| Contractor payments |  |

||

| Rewards | Discounts or cashback offered to customers as incentives for making purchases or participating in loyalty programs. | Cashback |  |

| Loyalty programs |  |

||

| Winnings | Monetary prizes awarded to individuals as a result of success in games of skill or luck. | Mobile gaming |  |

| iGaming |  |

||

| eSports |  |

||

| Expenses | Reimbursements made to employees for costs incurred while performing work-related activities. | Payroll |  |

| Spend management |  |

||

| Government disbursements | Payments made by government entities for use cases such as tax refunds, social benefits, or subsidies, or by government-funded NGOs for use cases such as refugee grants. | NGO programming |  |

| P2P transfers | Direct transfer of funds between individuals through digital platforms or mobile apps. | Communications/ Messaging app |  |

Why card payouts

Card payouts bypass many of the complexities posed by regional bank networks and deliver the flexibility and speed that bank payouts lack when serving cross-border needs. They simplify payout processes for disbursing businesses and accelerate the speed at which these payments are delivered to end-users – securing real-time payments delivery. This makes them especially valuable for companies transacting globally at scale.

Since most cards today are built into digital wallets (on Apple and iOS), payments made via card payouts are reflected in digital wallets. This optimises the payee experience by catering to user expectations in an increasingly digital world.

Card payouts are also very efficient in multi-sided contexts since they allow platforms to build and maintain a payments ecosystem whereby the same card method used for payment collection (of subscription or other usage-associated costs) can be filed and leveraged to issue payouts.

CARD PAYOUTS WITH RAPYD DISBURSE

Rapyd Disburse is a cross-border payments solution that lets businesses send payouts at scale to 190+ countries in 120 currencies.

Use Rapyd Disburse to unlock global card payouts for your organization.