Integrate multiple payment options across both in-person and digital channels to build a unified customer experience.

Omnichannel payments is a payments capability that allows for multiple methods to be integrated and synchronized across multiple channels to provide a unified commerce experience. This payments infrastructure complements a multi-channel sales strategy and is fit for merchants conducting business both in-person and online. It encompasses online and offline payments environments, and accounts for complementary modules like mobile apps, external hardware, and a centralized software. At Rapyd, omnichannel payments are part of the Collect product suite, which facilitates global payments acceptance via direct card acquiring and hundreds of alternative payment methods worldwide.

Building a Channel Mix

Many touchpoints are considered when building an omnichannel system. These physical and digital touchpoints facilitate transactional interactions with customers, and can include:

| Touchpoint | Description |

| Brick-and-mortar | The retail stores where in-person business is conducted and payments are processed largely through point-of-sale systems. |

| Mobile | Non-traditional retail settings – like pop-ups and markets – where payments are processed via portable terminals that enable on-the-go selling. |

| Online store | Owned digital storefronts with embedded checkouts that enable customers to pay through varied digital payments methods. |

| Marketplace | Third-party commerce platforms that enable merchants to list and sell inventory in a collective marketplace. |

| Mobile apps | Proprietary applications built to deliver a shopping experience optimized for mobile. |

| Social | Social platforms with embedded shopping experiences that allow customers to buy directly from business merchants in-platform. |

Designing an Omnichannel Experience

Deploying a multi-channel strategy requires designing a frictionless payments experience across all touchpoints. The entire shopping journey should be considered – from discovery to post-purchase. Customers shopping on mobile may later finalize their purchase online or in-store. They expect flexibility and that their payment options carry over – whether they buy online and pick up in-store, purchase in-store and opt for home delivery, or choose to return an online purchase in-store. Each of these scenarios must be supported by a unified payments infrastructure that allows transactions to be initiated in one channel and completed or modified in another. This means ensuring that there is transaction history visibility, seamless authentication and card-on-file support across channels, and flexible refund and exchange policies. By delivering on the promise of flexibility, a well-designed omnichannel experience enhances convenience, drives customer retention, and ultimately strengthens brand loyalty.

Thinking Omnichannel with Rapyd

Rapyd’s flexible APIs, pre-built SDKs, and plug-and-play solutions enable merchants and partners alike to design custom omnichannel experiences. Due to its modular nature, developers can pick-and-choose the components most relevant to the design of their payments experience.

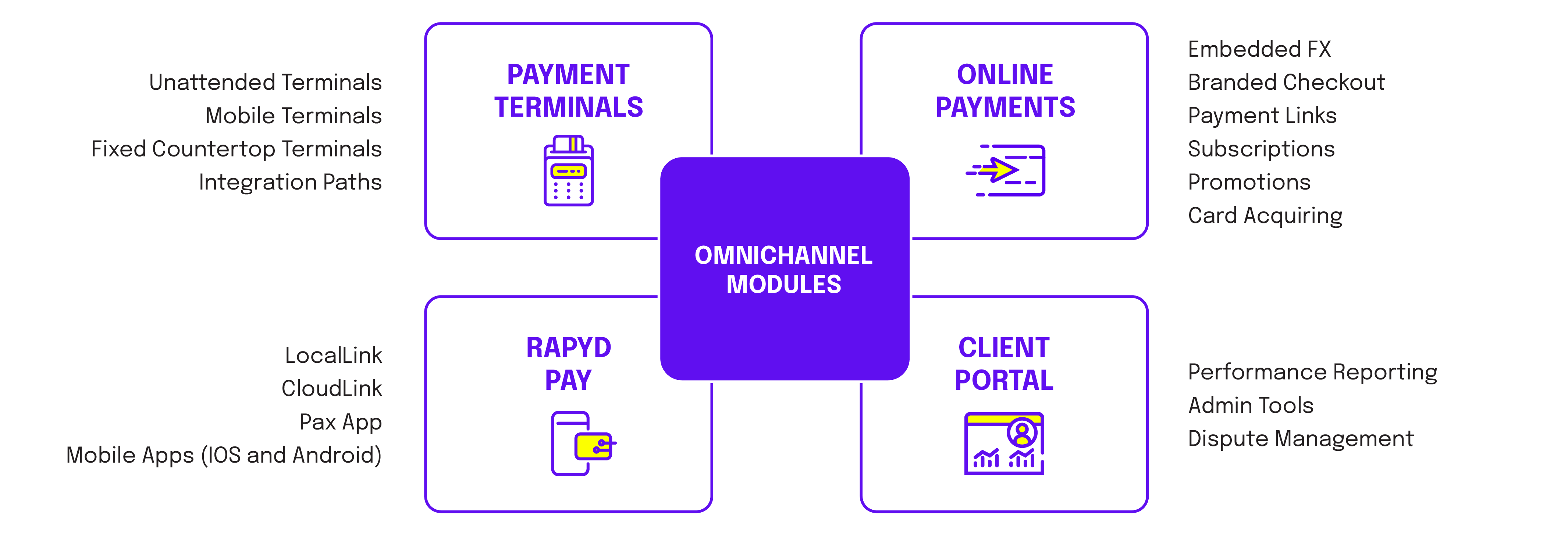

There are four key modules to Rapyd’s omnichannel solution:

- Online payments – capabilities that power digital checkout and payment experiences, powered by Rapyd’s direct acquiring licenses and global partner network.

- Payment terminals – Hardware devices (largely PAX) used to process in-person payments at retail or service locations.

- Rapyd Pay – Software apps (iOS, Android, PAX) that power in-person payment processing on payment terminals or compatible phones and tablets.

- Client Portal – a unified payments management platform for managing transactions, monitoring payment performance, and accessing value-add tools like dispute management.

Since these modules are complementary, at least one element from each should be leveraged when building an omnichannel payments experience.

Weighing the advantages of an omnichannel strategy

An omnichannel strategy delivers payment flexibility to customers and ensures they have a seamless experience when transacting across multiple channels. A single-channel approach risks creating silos and friction points that can lead to lost sales and lower customer satisfaction. The following table highlights key differences between the two:

| Multi-Channel Strategy | Single-Channel Strategy | |

| Checkout Experience | Allows for saved payment methods, faster checkout, and auto-filed details across channels. | Requires customers to reenter payment details at every channel encounter. |

| Payment Flexibility | Supports multiple payment methods (online, in-store, digital wallet). | Supports one payment method (online or in-person) reducing customer choice. |

| Cross-Channel Transactions | Enables transactions to start in one channel and be completed in another (i.e., buy online return in store) | Transactions are restricted to the purchasing channel, limiting flexibility. |

| Refunds and Exchanges | Allows seamless refunds and exchanges across channels. | Limited to the original channel. |

| Tokenization and Security | Network tokenization enabled across channels, protecting transaction data. | Security is often siloed, increasing friction in multi-channel interactions. |

| Recurring and Subscription Payments | Can unify recurring payments across channels. | May struggle to integrate subscriptions with one-time purchases. |

| Fraud Monitoring | Leverages data from multiple channel sources for fraud detection. | Fraud detection is isolated, leading to potential gaps. |