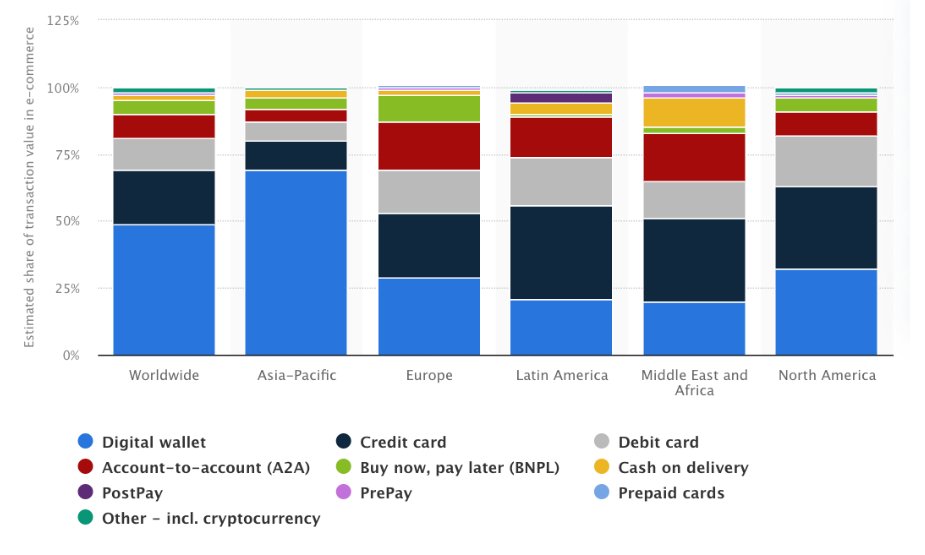

Why Accept Pay-By-Bank?

The pay-by-bank method is gaining momentum as a payment method preferred by both merchants and consumers. Rooted in open banking standards, Pay by Bank lets customers execute online payments directly from their bank accounts. This helps merchants with potentially lower fees and significantly diminishes the chances of chargebacks and fraud.

Customers opt for a “Pay by Bank” at checkout and are taken to their bank’s trusted online platform, where the transaction is approved and completed.

Advantages:

Cost Efficiency: Direct debit methods like “Pay by Bank” usually come with low transaction fees, making it more profitable for merchants.

Chargeback Protection: The threshold for initiating disputes is higher with “Pay by Bank”, giving merchants a stronger say in refunds. This is especially important for industries, like online gaming, and that experience a high number of Chargebacks.

Fast Transactions: In many countries, like the U.K. and Singapore, pay-by-bank combines with real-time payment networks, so merchants receive payment almost instantaneously.

Consumer Trust: Transactions via their bank’s interface enhance customer trust, especially for cross-border commerce.

Disadvantages:

Bank Dependency: Any technical glitches or downtime at the bank can impact transactions.

Limited Familiarity: Some customers might not be acquainted with this payment method.

Why Accept Buy Now, Pay Later Payments for eCommerce?

Gaining popularity, Buy Now, Pay Later (BNPL) allows consumers to purchase immediately and settle the bill in installments. This model empowers consumers with financial flexibility and encourages them to complete purchases they might otherwise abandon. Businesses like Kontempo have leveraged this trend, partnering with Rapyd to enhance their payment offerings.

Advantages:

- Flexibility: BNPL offers consumers the freedom to manage their finances on their terms. They can secure a product immediately and spread the cost over a period, making high-ticket items more accessible.

- Increased Sales: For merchants, BNPL can be a game-changer. By offering this payment flexibility, businesses often witness higher cart values, reduced cart abandonment and improved conversion rates.

Disadvantages:

- Debt Risk: While BNPL offers flexibility, it also comes with responsibility. Consumers who overextend themselves might find it challenging to keep up with payments, leading to potential debt accumulation.

- Fees for Merchants: BNPL solutions often come with higher fees for merchants. Merchants must weigh the advantages vs the costs to decide if BNPL is right for them.

Localize Payment Options for More Sales

According to Fintech Journal PYMNTS, “eTailers offering local payment options generate 22% more in regional revenue than those lacking these options, yet just 1.8% of merchants believe that customers desire these local methods.”

In global ecommerce, understanding and adapting to regional nuances is critical. These payment methods can range from local Digital Wallets like Paytm in India and GrabPay in Singapore to real-time payment networks like PIX in Brazil to accepting Diners Club credit cards in Latin America. With Rapyd, you can localise checkout with more than 900+ payment methods, ensuring your ecommerce purchase experience always feels local.

Advantages:

- Localised Experience: Offering local payment methods ensures that businesses cater to the unique preferences of consumers in specific regions, building trust and enhancing the overall user experience.

- Higher Conversion Rates: When consumers see familiar payment options, they’re more likely to complete their purchase. This can lead to reduced cart abandonment and higher sales.

- Broadened Market Reach: By embracing a variety of local payment methods, businesses reach market segments that might otherwise be inaccessible.

Disadvantages:

- Integration: Offering local payment methods can require integrating with and managing multiple ecommerce payment processing companies. Working with a company like Rapyd can simplify global payments.