How Do Credit Card Payments Work for Merchants?

When most people think of credit card payment processing, they think of a card scheme, which is a payment network that uses cards, like Visa or Mastercard. But completing a successful credit card transaction in seconds involves a series of actions and an entire ecosystem of players that merchants should understand.

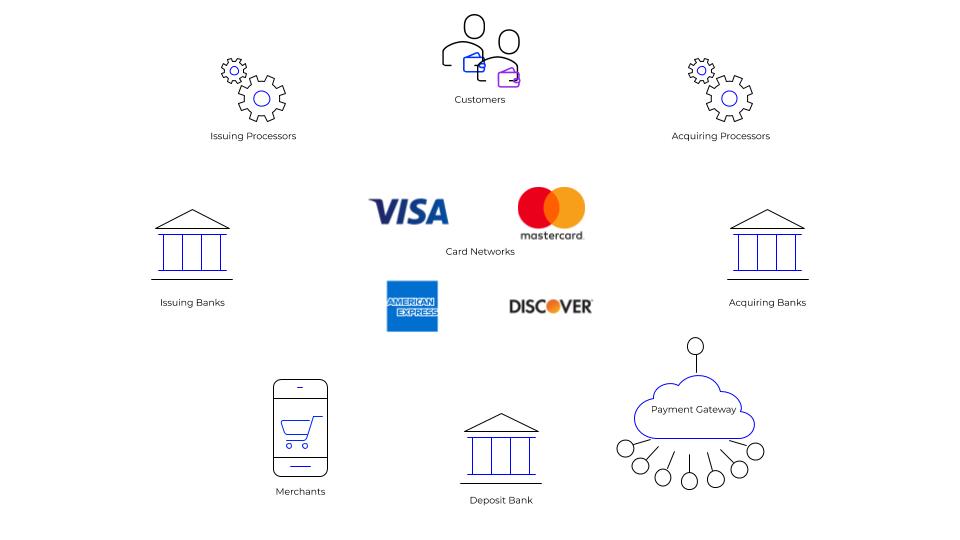

The Credit Card Payment Processing Ecosystem

Common Credit Card Payment Processing Terms and Definitions

Card Scheme

Visa, MasterCard, American Express and Discover are among the largest card schemes, also referred to as card networks or card brands.

Visa and Mastercard are both open networks and actively encourage banks to issue their cards to consumers and to acquire or accept transactions using cards. There is no direct relationship between the card schemes and card holders. Issuing and acquiring banks must follow the operating regulations created by the card networks. There are fines for non compliance that acquirers pass on to merchants. The card schemes collect fees from acquirers who are reimbursed from merchants.

Amex is a closed network. It acts as the card issuer and the card acquirer and has a direct relationship with the consumers and the merchants.

Discover has a hybrid model, issuing the cards directly to consumers, but allowing banks to act as acquirers to settle directly with the merchants.

Local Card Schemes Many countries are home to local card schemes that are preferred by regional consumers, these include BC Card in South Korea, Rupay in India, and JCB in Singapore.

Issuing Bank

An issuing bank issues credit cards to consumers on behalf of the card networks (Visa, MasterCard). Issuing banks front the funds to merchant accounts when someone pays with a credit card. This carries a degree of risk – If a cardholder defaults the issuing bank takes part of the hit, which is why they charge a per-transaction fee.

Acquiring Bank

The acquiring bank deposits funds from credit card sales into a merchant’s account. An acquiring bank or “merchant bank” manages and underwrites the merchant account that enables the merchant to accept credit and debit cards. In doing so, the bank carries the same risk as issuing a line of credit and is ultimately on the hook for any consumer disputes should a merchant that they sponsor go out of business.

Payment Processor

Acquiring and issuing banks do not have the infrastructure to connect directly to a payment network. A third-party payment processor connects the merchant and the financial institutions to authorize transactions and facilitate the transfer of funds. The functionality and value added services offered by payment processors can differ significantly.

Credit Card Payment Gateway

Integrating directly to a single payment processor is difficult. In many cases a company will leverage multiple payment processors and will need to maintain certification. A payment gateway provides a single interface that connects with multiple processors and also offers other value-added services, including tax calculation, payment tokenization, hosted payment pages, mobile SDK, 3D Secure, and fraud management to minimize PCI scope.

Payment Service Provider (PSP)

Payment Service Providers work with merchants and acquiring banks to simplify and manage the entire payment process – with many having their own gateways. By offering merchants software and APIs to collect and manage their payments efficiently, merchants can improve the payment experience for their customers. There are also additional benefits to working with a Payment Service Provider including security, currency processing and transaction reporting.

Rapyd is an example of a payment service provider. By giving merchants access to cards and alternative payment methods in 100+ countries, Rapyd provides a comprehensive solution to grow sales globally.