Credit Cards

As with consumer transactions, credit cards are a widely used payment method by businesses, albeit less so for large-ticket items or invoices.

Pros: Simplicity. Using credit cards for smaller business transactions allows for quick, easy, and protected payment when you need it. Additionally, making payments with credit cards is low-burden, since the payer is not responsible for fees.

Cons: Unfortunately, credit cards are not necessarily an ideal option for either large-ticket items or, often, for payees overall. While credit card companies may be thrilled to handle a $150,000 transaction because of the handling fees they will collect, the receiver can incur processing fees that can be nearly 3% of the purchase price. This makes credit cards a costly option for those receiving payments.

Often used for: Smaller purchases and subscriptions.

Global ACH

ACH, which stands for “automated clearing house,” transfers are considered invaluable payment methods for businesses for being able to pay obligations such as payroll, or moving large sums of money at once. Bank transfers are also an attractive payment method for many businesses making a purchase that exceeds credit card limits, and for facilitating online transactions with international customers. Using bank transfers for transactions also simplify payments by virtue of automatic account deductions, reducing effort on the customer’s behalf. Finally, bank transfers remove the risk of chargeback fraud which is inherent with credit card transactions.

Pros: ACH is a reliable and robust model. The global reach of ACH transfers is also significant; most countries have similar clearing house technology in place, making it a more universally embraced payment method.

Cons: The ACH method necessitates roughly two to three days of processing time and it is not perfect: Payments can and do get lost on occasion, and take longer than other options available.

Often used for: payroll, large expenses, recurring payments and subscriptions, international payments, payouts

Real-Time Bank Transfers

ACH transfers are reliable, but slow – sometimes taking up to two weeks for international transactions. Many countries have implemented faster payment rails that enable near real-time funds transfers in an effort to reduce processing time and allow businesses and individuals to send and receive money quickly. Common systems enabling real-time transfers include Faster Payments in the United Kingdom and UPI, or Unified Payments Interface, in India.

Pros: Speed! With processing times reduced down to seconds, funds can be paid out and received by businesses almost instantly, creating less burden of effort for the payer and immediate payout for the organization or person receiving funds. Such models are popular in areas where they are accessible; in its first three years, UPI in India transacted a total of $240B USD over 1,000 transactions. (The Hindu Business Line)

Cons: The downsides to Real-Time Bank Transfers center around limits and accessibility. With these systems, there are often caps on transfers (100,000 ₹ for UPI and £250,000 in the UK) limiting payments on very large expenses. Additionally, there are limits to accessibility; one must use a bank inside the network in order to benefit from transactions in real-time.

Often used for: mid-range expenses, B2B transactions in countries with real-time bank transfers, real-time payouts to workers and suppliers.

Wire Transfers

Also popular for large sums of money, the wire transfer is reliable and well-known globally.

Pros: The most important benefit of a wire transfer is speed. Wire transfers occur more quickly than ACH payments, while still being able to satisfy payments of a large size. Wire transfers (also known in the banking industry as “rails”) are used much more widely on a global level.

Cons: In exchange for speed comes increased cost. While they are a reliable way to transact large sums of money, there are costs associated with doing so, making them only one of several payment method tools a business should be equipped to use.

Often used for: Wire transfers are often favored for large expenses when speed is critical, especially for cross-border and international B2B Payments.

Checks

For organizations doing business in the US, checks are still a common way to both make and receive payments.

Pros: Ease of use, particularly within the United States. If a payment needs to be made, you can simply drop a check in the mail and be done with it, relieving the payer of much of the burden. Because of the ubiquity of bank accounts within the US, as well as the infrastructure in place to move checks, checks remain the most prevalent payment method used by businesses stateside.

Cons: Checks can be time-consuming, inefficient, and easily lost in the mail. There is also a higher rate of fraud with checks than with other forms of business payment.

Often used for: Contractor payroll, vendor invoices

B2B Payments Are Due for Greater Digitization

The B2B Payments Landscape is evolving. Businesses must be equipped to handle a variety of different transaction types across different global locations and make everything work across disparate systems. Because there is not yet a uniform way to approach all of these transactions, the B2B payments world can feel unstructured and due for an update. ACH technology, for instance, is over 50 years old. CFOs, controllers, treasurers, and decision-makers are all stakeholders that need to move their business to better, faster and more cost-effective payment solutions as their businesses transact more online and globally. Newer generations of business buyers do not have the time or patience to deal with analog procurement systems, necessitating rapid change in digitization. Robust B2B payment solutions can provide a variety of locally preferred payment methods to business customers at global scale, integrate with your websites, apps and systems, provide comprehensive fraud monitoring and streamline operations.

Leverage a Global Payments Network to Simplify B2B Payments and Payouts

The Rapyd Global Payments Network enables B2B solutions to accept and send funds using the right payment methods across different transaction types and regions. Explore countries and payment methods available through the Rapyd Global Payments Network to learn if it is the right solution for your business.

Sources:

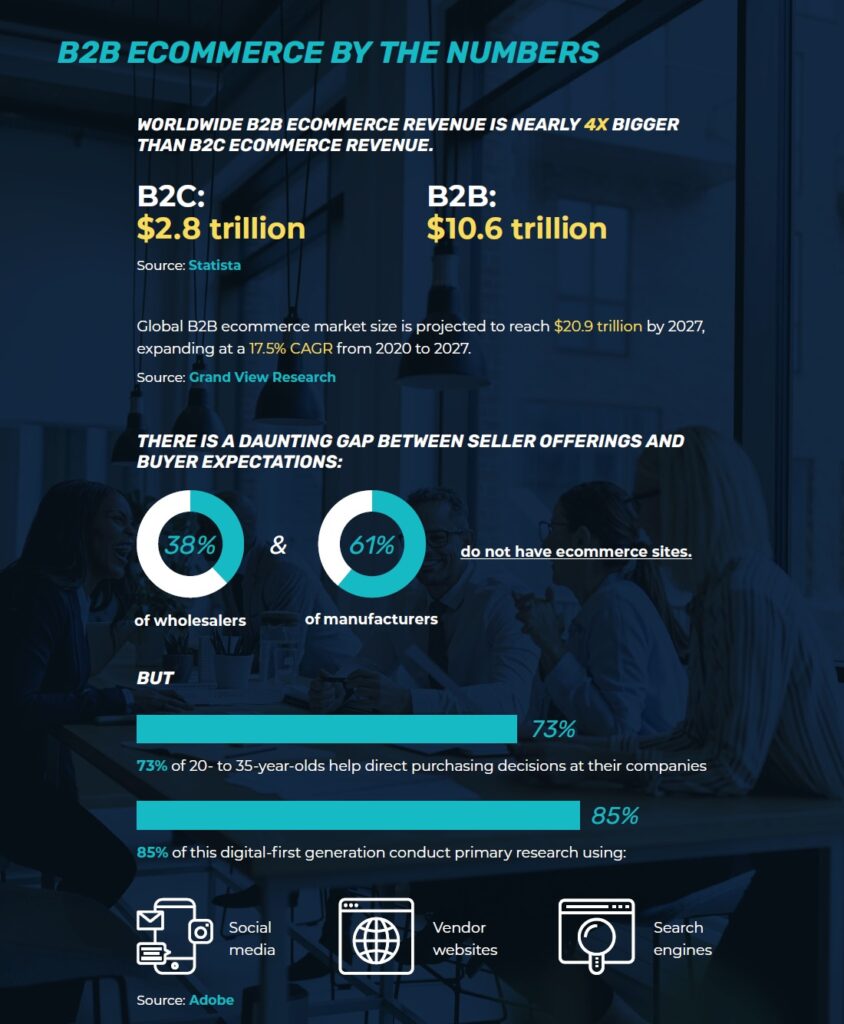

Adobe. (2020). B2B eCommerce by the Numbers. Infographic

Due. (2017, 1 26). State of Invoicing for 2017. Due. https://due.com/blog/state-invoicing-2017/

The Hindu Business Line. (2020, 9 1). UPI completes 1,000 cr transactions. The Hindu Business Line. https://www.thehindubusinessline.com/info-tech/upi-completes-1000-cr-transactions/article29339816.ece